Harrow: The Hidden Engine Behind One of Ophthalmology’s Fastest-Growing Companies

A deep look at how Harrow is building a durable position inside ophthalmology’s workflows, what’s driving its growth, and what the next decade may reveal

This review of Harrow Inc. represents the culmination of several years of watching the company sharpen its position inside ophthalmology and expand into a broader branded footprint. The work here draws from full financial statements, transcripts, product-level data, competitive landscaping, and extensive valuation modeling. A position has been built over time with a blended cost basis near $26 after multiple lots taken from the $8 range upward, and this analysis reflects both the strengths observed and the areas that still demand scrutiny.

Part 1 focuses on how Harrow actually operates, why ophthalmology behaves differently than most healthcare markets, and how the company’s distribution footprint and product breadth translate into durable economics.

Part 2 shifts from narrative to numbers, focusing on owner’s earnings, valuation scenarios, and what the current stock price already assumes.

Why Ophthalmology Is One of the Most Misunderstood Markets in Healthcare

Most investors approach Harrow as if it were a standard specialty pharma company. It really isn’t. Ophthalmology runs on a different logic entirely.

It’s a procedure-driven field where everything depends on timing, predictability, and the ability to keep high-volume clinics moving without interruption. Cataract surgeons often work through 20 to 30 cases a week. Retina specialists might handle 40 to 70 injections a day. Even the routine in-office procedures stack up quickly.

In that world, a small supply issue doesn’t just create a minor inconvenience. It can derail a full day’s schedule, frustrate patients, disrupt staff flow, and throw an ASC (Ambulatory Surgery Center) off balance. Retina injection clinics operate almost like industrial lines—any slowdown creates ripple effects for hours.

This dynamic has nothing in common with oncology, primary care, or cardiology. Ophthalmology rewards vendors that make life easier for practices. The companies that win are the ones that keep workflows smooth, get products where they need to be on time, maintain reliability, respond quickly, and reduce the day-to-day friction that surgeons and ASC managers deal with.

That is the environment Harrow grew up in. It’s also why the company gets misunderstood. Most analysts miss Harrow because they miss how ophthalmology actually works.

The Real Layout of the Market Harrow Serves

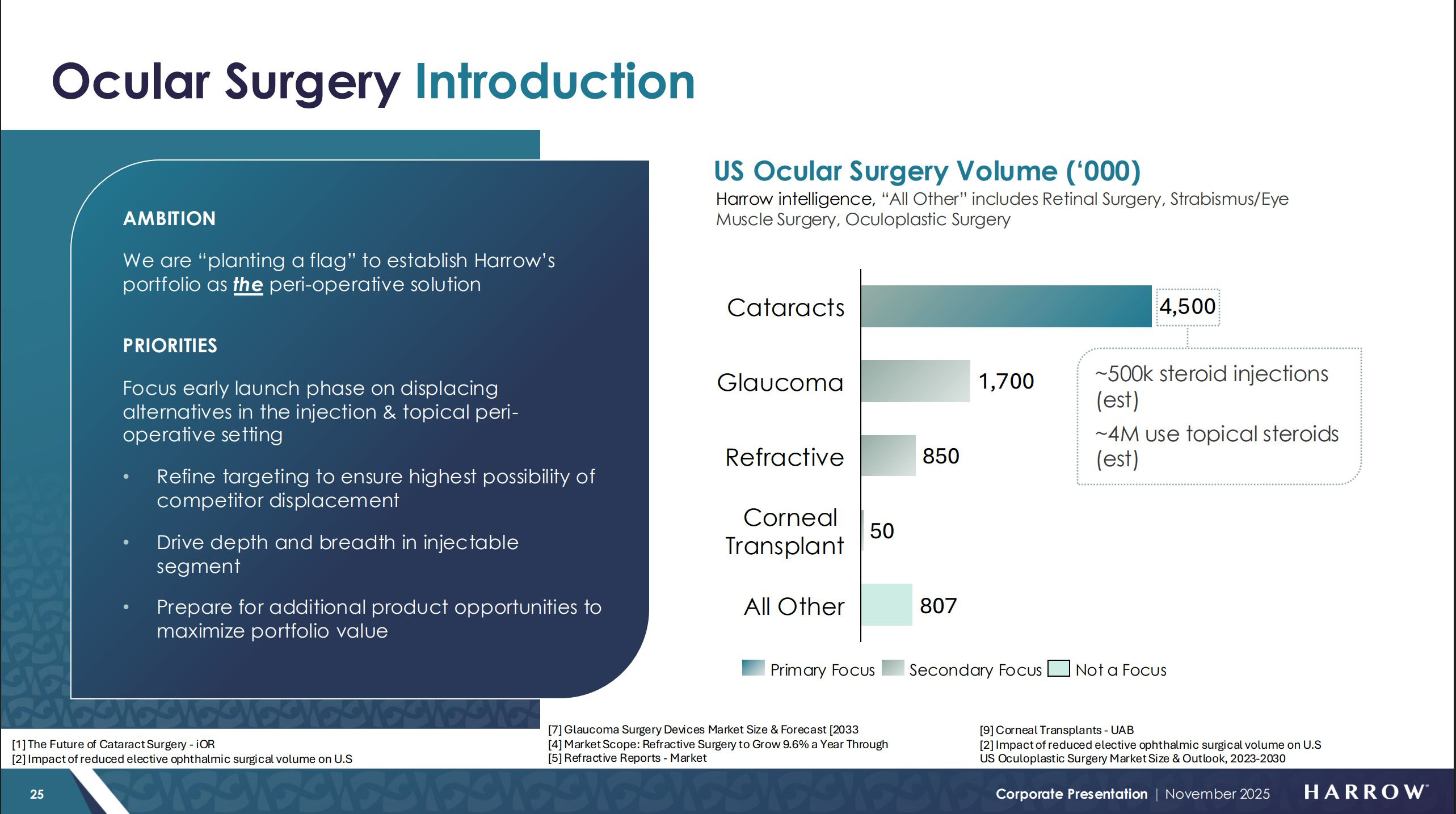

Ophthalmology is often treated as a single category, but the specialty functions more like five connected ecosystems with their own rules and pressures:

Cataract surgery

Retina and back-of-the-eye disease

Glaucoma

Dry eye and ocular surface disease

In-office therapeutics and diagnostics

Each of these areas operates with its own reimbursement dynamics, workflow bottlenecks, patient volumes, and vendor frustrations. A company that expects ophthalmology to behave like traditional pharmaceuticals will miss how the specialty really works.

This distinction matters because Harrow is not pursuing a single breakthrough therapy that sits in only one of these segments. The company builds and acquires a portfolio that spans nearly every room where ophthalmologists spend their time. The strategy generates multiple touchpoints within the same practice, opens up cross-selling opportunities, raises customer stickiness, and reduces the dependence on any one drug. It also creates a more predictable path for long-term growth.

In practical terms, a cataract surgeon might rely on:

compounded intraoperative drops

branded anti-inflammatories after surgery

branded antibiotics

dry-eye therapeutics for pre-operative optimization

diagnostics for screening and follow-up

and, in the near future, Melt-300 for sedation

Once Harrow becomes part of a practice’s workflow, it is difficult to displace.

Why Big Pharma Stepped Back and Why Harrow Stepped Forward

For years, ophthalmology was dominated by large pharmaceutical companies. Products like Lucentis from Genentech, Eylea from Regeneron, Durezol from Alcon, Restasis from Allergan, Lotemax from Bausch and Lomb, and Xalatan from Pfizer defined the space.

Over time, margins tightened and the operational demands of the specialty increased. Larger companies began moving away from many ophthalmic assets because the effort required to support them exceeded the return. Ophthalmology is highly fragmented, with thousands of independent practices, a mix of clinics and ASCs, heavy procedure volume, and reimbursement dynamics that require constant attention. It is a specialty that rewards hands-on execution rather than broad national marketing strategies.

The business model Big Pharma prefers looks very different. Large companies aim for concentrated revenue from large health systems, blockbuster therapies with high revenue per customer, centralized purchasing decisions, and slow, predictable sales cycles. Ophthalmology is the opposite. It is a market defined by small practices, rapid patient flow, constant scheduling pressure, and a high expectation of responsiveness from vendors.

As a result, large companies gradually stepped away from many of the smaller ophthalmic products and older branded assets that still mattered to surgeons but no longer fit corporate priorities.

Harrow recognized the opportunity. The company built a strategy around the parts of the market that were overlooked, operationally demanding, and still essential to everyday clinical practice.

The Three Pillars Behind Harrow’s Growth Engine

Harrow operates three distinct but interconnected businesses that reinforce one another:

ImprimisRx, the ophthalmology-focused compounding and outsourcing pharmacy

A growing portfolio of scalable branded pharmaceuticals

A small but meaningful set of strategic options through its equity holdings and licensing relationships

Each pillar serves a different role. Together they form the operating flywheel that drives Harrow’s long-term trajectory.

Pillar One: ImprimisRx, the Backbone of the Ecosystem

ImprimisRx is one of the largest compounding businesses dedicated exclusively to ophthalmology in the United States. Its position in the market is unusual. Surgeons and practices reorder frequently, depend heavily on reliable delivery, and often use custom formulations that are tailored to specific procedures. Over time, this has created deep loyalty and regular contact with thousands of practices.

Most pharmaceutical companies struggle to get consistent access to clinics. ImprimisRx has that access by default. The business is inside the workflow every week, which creates a type of distribution advantage that is difficult for larger companies to replicate.

ImprimisRx does more than generate revenue. It acts as infrastructure. It provides ongoing visibility into practice needs, early awareness of clinical pain points, and a natural channel for introducing branded therapeutics. It smooths adoption curves for new products, including Melt-300, because the trust is already established. In many ways, it gives Harrow the credibility and operational reach that large companies often lack.

This is the foundation of Harrow’s model. The compounding business funded the early years, built the distribution network, and continues to support every branded product the company brings to market.

“ImprimisRx products continue to provide stable recurring revenue, generating approximately twenty point one million dollars in revenue in the third quarter.”

— Andrew Boll, CFO, Q3 2025 earnings call

Pillar Two: The Branded Portfolio as the Margin Expansion Engine

Harrow’s branded portfolio fills the gaps abandoned by larger pharmaceutical companies. The company focuses on acquiring off-patent ophthalmic drugs, under-promoted brands, and smaller assets that no longer fit the priorities of major manufacturers. These products are often clinically useful but operationally neglected, and they tend to underperform inside large organizations that depend on blockbuster-scale revenue.

Inside Harrow, the same assets behave differently. The company already has the distribution network, the practice-level relationships, the weekly shipping cadence, and the trust that comes from years of reliable service. A product that may have been insignificant within a large global portfolio can become meaningful when supported by a company that specializes in ophthalmology and has direct access to the clinicians who use it every day.

The branded products carry higher margins than compounding and benefit from the infrastructure already in place. They increase operating leverage, broaden customer penetration, and diversify the revenue base. Because Harrow maintains such a wide footprint within the specialty, each newly acquired drug has a higher probability of rapid adoption compared with a company that would need to build relationships from scratch.

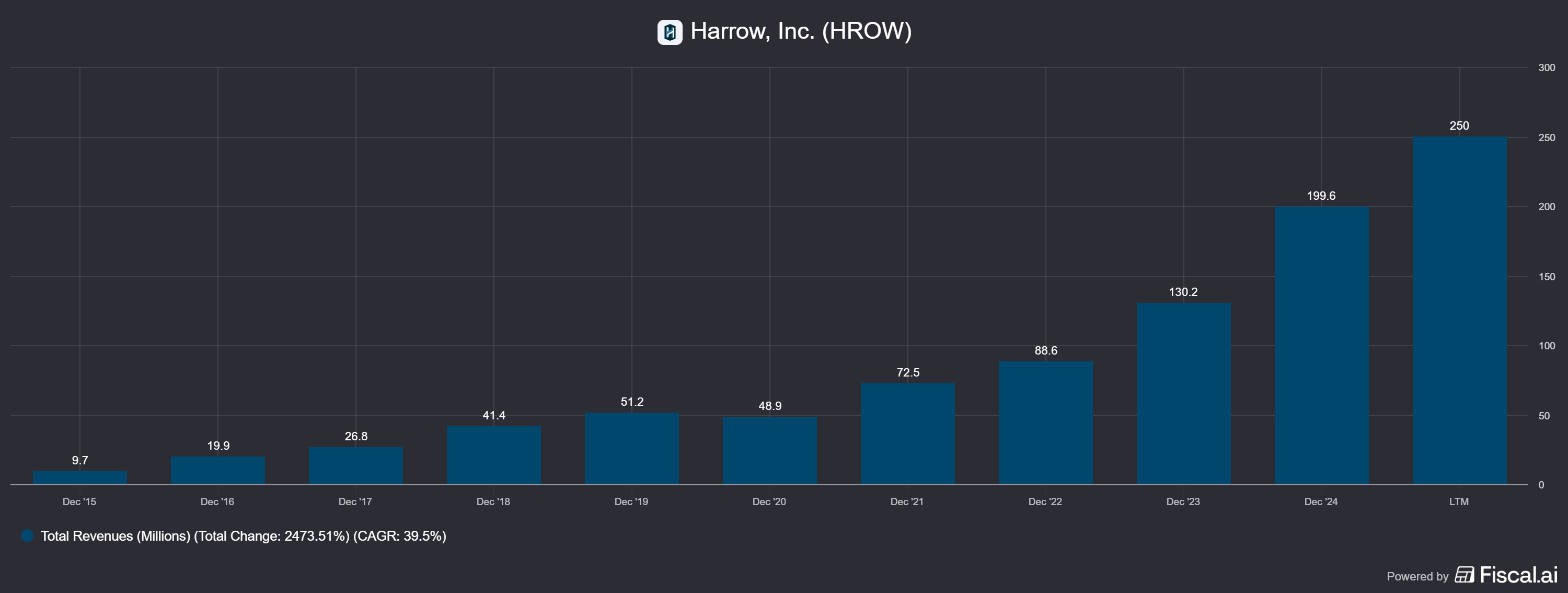

This strategy is a major reason the company has grown from roughly twenty million dollars in revenue a decade ago to two hundred fifty million dollars today. The progression has been steady, and none of it depended on a single blockbuster launch. The portfolio approach is the real driver of long-term growth.

Exhibit: What Harrow’s Branded Portfolio Actually Includes

Harrow’s branded portfolio covers a wide range of ophthalmic needs. According to the company’s investor materials (the same set underlying IHEEZO and VEVYE launches), the branded suite currently includes:

Anti-inflammatory / Pain

• IHEEZO – lidocaine ophthalmic gel approved for ocular anesthesia

• Durezol – corticosteroid for post-operative inflammation

• Triesence – injectable steroid used in retinal procedures

Dry Eye / Ocular Surface

• VEVYE – cyclosporine 0.1% for chronic dry eye

• Iyuzeh (latanoprost) – preservative-free prostaglandin

• Zerviate – antihistamine for allergic conjunctivitis

Anti-Infectives / Perioperative

• Maxitrol – antibiotic + steroid combination

• AzaSite – azithromycin ophthalmic solution

• Natacyn – antifungal for rare corneal infections

Other Portfolio Assets

• DEXYCU – dexamethasone intraocular suspension

• Flarex / FML / Moxeza – established ophthalmic therapies

• Several legacy branded products acquired from Novartis, Alcon, B+L and Santen

Harrow’s strategy is not about placing big bets on any one product. It is about scaling a portfolio that integrates naturally into the daily workflow of ophthalmology, especially post-operative care, chronic surface disease, and perioperative therapy.

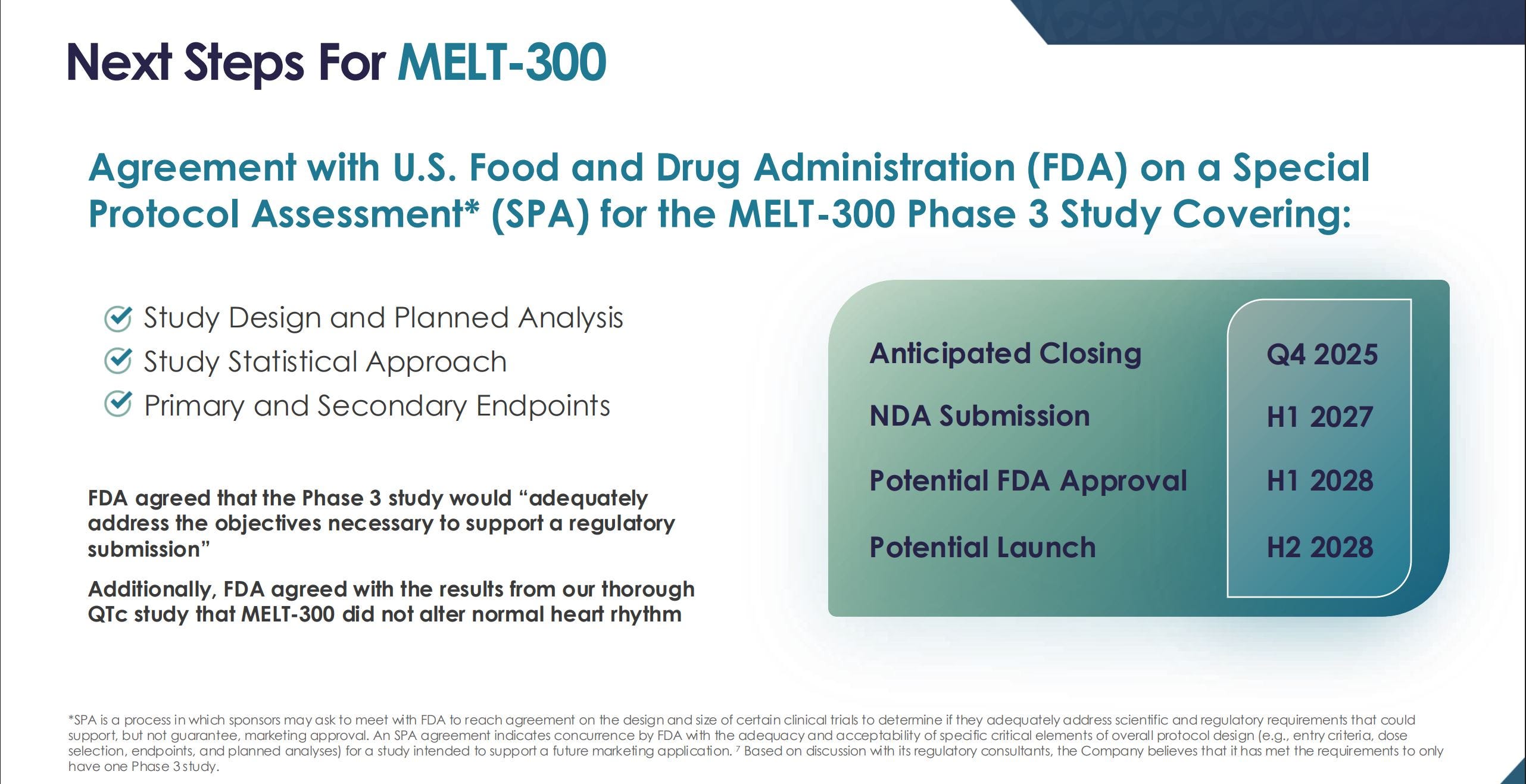

Pillar Three: Optionality Through Melt-300 and Related Assets

Harrow also maintains a small but important optionality layer. This includes minority stakes in Surface Ophthalmics, royalty rights tied to Surface’s pipeline, equity and royalty rights connected to Melt Pharmaceuticals, and now full ownership of Melt-300. These positions provide exposure to clinical upside without requiring the balance sheet risks that typically accompany traditional biotech development.

The design is intentionally asymmetric. Harrow contributes limited capital, absorbs minimal clinical risk, and retains the ability to use its commercial footprint to maximize downstream value. When one of these assets reaches commercialization, Harrow is in position to control the launch and accelerate adoption through relationships that already exist.

This structure sets the stage for Melt-300, which has the potential to reshape workflow inside ambulatory surgery centers.

Melt-300: A Workflow Product Hidden in Plain Sight

At its core, Melt-300 is a sublingual sedation and anesthesia tablet designed for ophthalmic procedures. Its purpose is straightforward. It replaces the need for IV sedation.

Eliminating the IV line removes several of the biggest bottlenecks in cataract surgery. IV sedation requires an additional nurse, IV setup materials, patient preparation, and continuous monitoring. In many high-volume surgical centers, the surgeon is not the limiting factor. The constraint is anesthesia readiness and the time consumed by IV placement, movement, and monitoring.

Melt-300 reduces those steps. It shortens patient preparation, lowers staff requirements, improves throughput, and reduces the risk of IV-placement delays. The economic impact can be meaningful. Additional surgical slots open up, staff can be redeployed, and cases move more smoothly through the operating room.

This is fundamentally a workflow solution rather than a traditional drug launch. It fits directly into Harrow’s strategy because it improves the economics of an ASC and embeds the company deeper into one of the most critical points of the ophthalmic workflow.

Melt-300 Is Much Larger Than Ophthalmology

Although Melt-300 is being developed for cataract surgery, the addressable opportunity is broader. At the December 2025 Piper Sandler Healthcare Conference, Mark Baum highlighted that more than 90 percent of cataract procedures today require IV fentanyl, and that reducing opioid exposure is a core part of the product’s value. But he also emphasized something far more expansive: the same sedation challenges appear across multiple specialties.

Dental procedures, dermatology, plastics, GI endoscopy, and even MRI environments routinely rely on sedatives to keep patients comfortable, especially where anxiety or claustrophobia interrupt procedures. Melt-300’s sublingual strategy aligns well with these high-volume use cases.

This positions Melt-300 not as an ophthalmology-only drug, but as a potential workflow enhancer across several outpatient specialties. The intellectual property estate supporting Melt-300 spans U.S. and international jurisdictions, which gives Harrow optionality well beyond the initial cataract indication. Even modest multi-specialty adoption increases the long-term value of the platform.

Source: Piper Sandler Healthcare Conference, Dec 2025 (Mark Baum)

Why Melt-300 Matters to Investors

Melt-300 is not a traditional biotech swing aimed at producing a blockbuster drug. Its importance comes from how it amplifies the structure Harrow already built. The product strengthens the company’s branded portfolio, reinforces the value of ImprimisRx through increased cross-selling, deepens practice-level loyalty, and raises Harrow’s relevance inside cataract surgery. It also supports margin expansion and increases the level of dependence ambulatory surgery centers have on Harrow as a workflow partner.

Even moderate adoption can shift the company’s growth trajectory. The key point is that Harrow does not need Melt-300 to justify its current valuation. The existing business already supports the numbers. Melt-300 simply increases the probability and potential size of the upside.

A Second Asset: Melt-210 as an Underappreciated Optionality Layer

Harrow also disclosed a second sedation product, Melt-210, an orally dissolving midazolam tablet with rapid onset and offset. Baum described it as a “hidden gem,” highlighting broad use cases across dental work, dermatologic procedures, vasectomies, GI procedures, and MRI exams where anxiety often disrupts care. Today, midazolam is typically delivered as an IV or a syrup, both of which are suboptimal formats. An orally dissolving tablet with predictable kinetics would represent a meaningful improvement in convenience and safety across tens of millions of potential use cases.

Melt-300 anchors Harrow inside the ASC. Melt-210 expands the addressable market far beyond it.

Source: Piper Sandler Healthcare Conference (Melt-210 discussion)

How Harrow Compounded from Twenty Million to Two Hundred Fifty Million

The path from $20M in revenue to $250M dollars over roughly a decade was not driven by a single breakout product. Instead, Harrow built a compounding engine by recognizing a neglected segment of the market and becoming essential to the practices within it.

The company began by focusing on ophthalmic compounding, a part of the specialty that required reliability, speed, and constant contact with clinicians. That foothold created a distribution network that other companies struggled to match. Harrow then began acquiring branded assets that were under-promoted or mismanaged by larger companies. Once inside Harrow’s system, these products benefited from stronger access, improved reliability, and a customer base that already knew the company well.

This strategy was repeated across multiple assets. Along the way, Harrow added selective optionality through equity and royalty positions in Surface and Melt, and continued reinvesting in commercial capabilities. The result was a steady, multi-year progression that reflected consistent execution rather than dependence on a single event.

It takes a different path than the usual compounding story, but the trajectory builds the same way over time.

Why Harrow’s Distribution Footprint Is the Real Moat

Most pharmaceutical moats are built around patents, data exclusivity, or a single dominant therapy. Ophthalmology operates on a different plane. Reliability is the real currency. Practices move fast, schedules tighten without warning, and a single disruption can throw a surgical day into disarray. Any partner that keeps those systems steady earns a level of trust that compounds year after year.

Harrow’s distribution footprint has grown into that role. The company shows up in the places that matter, with the consistency that practices depend on. The commercial team has spent years inside clinics and ASCs, learning how each one works. ImprimisRx delivers on a cadence that allows surgeons to focus on the patient in front of them rather than worry about what might not arrive tomorrow. High fill rates and dependable customer support turn into something larger than individual transactions. The relationship becomes part of the workflow.

The moat takes shape through these repeated interactions. It is built from trust, reliability, and the comfort that comes from knowing a vendor has already handled the problem before it becomes a crisis. It forms as more products enter the portfolio, as practices lean on Harrow for a broader set of needs, and as competitors choose not to enter the parts of ophthalmology that require this level of operational attention.

Infrastructure rarely draws attention when it works well. It becomes visible only when it fails. Harrow has become the company that keeps the system running quietly in the background. That is the foundation behind everything else the business has built.

What Will Shape Harrow’s Next Ten Years

Several forces will guide the next stage of Harrow’s evolution.

1. A shift toward higher-margin branded products.

As the portfolio continues to tilt in that direction, margins improve and cash generation strengthens.

2. The full rollout of Melt-300.

Its value comes from how it simplifies workflow in the surgical setting and opens new points of connection inside the practice.

3. Deeper integration within each practice.

When a company provides solutions across multiple steps of a clinician’s day, it becomes harder to replace.

4. More leverage from the existing distribution network.

The infrastructure already in place lowers the cost and difficulty of bringing each new product to market.

5. A steady opportunity to add new assets.

Harrow can continue acquiring ophthalmic products because each one enters a footprint that is already trusted.

6. Operating leverage as working capital settles.

Receivables and inventory cycles have a path to normalize, which supports the longer-term financial picture.

7. A specialty that still lacks committed attention from larger pharmaceutical companies.

The same gap that allowed Harrow to scale remains open. Most large firms continue to avoid the high-touch demands of ophthalmology.

What Could Disrupt the Flywheel and How to See It Early

Every company carries real risks, and Harrow’s can be monitored without guesswork. None of these are abstract. They show up in the numbers and in the day-to-day execution. The key is watching the pressure points before they build into something larger.

1. Leverage pressure

Harrow operates with meaningful net debt, and interest coverage remains tight. The model works as long as execution stays consistent. Any prolonged stumble would reduce flexibility.

2. Working capital volatility

Receivables have been elevated, and normalization is important over the next few quarters. This is a solvable issue, but it affects cash conversion until it settles. Stabilization here is one of the clearest signals of long-term financial strength.

3. Product execution risk

New branded assets must integrate smoothly into the commercial system. Harrow’s distribution footprint helps, but each product still needs careful onboarding. Execution quality matters more than product count.

4. Reimbursement sensitivity

Some branded items depend on reimbursement stability, particularly when CMS makes adjustments. These changes do not break the model, but they influence near-term performance.

5. Commercial bandwidth strain

Expanding the portfolio too quickly risks stretching the commercial team. Maintaining focus is essential. A wide footprint only works if each product receives the attention required to scale properly.

6. Melt-300 adoption curve

The long-term thesis does not depend on Melt-300 becoming a blockbuster. However, the slope of adoption influences the growth trajectory. Slower uptake would not undermine the business, but it would shift the pace at which the flywheel accelerates.

The balance here resembles a disciplined martial-arts practice. The strength comes from steady form, consistent repetition, and focus on fundamentals. When those fundamentals remain intact, the system continues to compound.

The Real Harrow Story and Why Most Investors Miss It

Harrow is often analyzed through the wrong lens. Many investors approach the company looking for blockbuster-level science, traditional biotech milestones, binary FDA events, or EPS screens that penalize amortization. That framework does not fit the business. Harrow is not built like a classical biotech or a single-asset pharmaceutical company.

The company operates as a workflow partner, a distribution platform, and a portfolio owner. It grows by solving practical problems inside clinics and surgery centers, delivering reliably, and strengthening relationships over time. Its success comes from execution rather than scientific breakthrough, and from consistency rather than volatility.

That approach has allowed Harrow to compound revenue for more than a decade. The same operating discipline positions the company for meaningful opportunities ahead.

Management: The People Behind the Flywheel

Harrow’s strategy only works because the leadership team understands something most companies never bother to learn: ophthalmology is an execution sport. It rewards consistency, responsiveness, and long-term trust far more than flashy science or oversized sales forces. Harrow’s management team has spent more than a decade building credibility in the exact corners of the specialty where reliability is everything.

Leadership Philosophy

The company has always been run with an operator’s mindset. Instead of chasing moonshots, the team focuses on removing friction for practices, solving the problems that slow surgeons down, and earning the kind of goodwill that compounds over years. This shows up in the call transcripts, in how customers describe their interactions with the company, and in how Harrow behaved during the periods when supply chains across the industry were strained. Practices remember who delivered for them when others didn’t.

Mark Baum’s Approach

Mark Baum remains the defining force behind Harrow. His style is straightforward: find overlooked assets, rebuild reliability, distribute them through a footprint that others can’t replicate, and reinvest aggressively into the parts of the business that deepen customer trust. He talks more like a founder-operator than a biotech CEO, which is exactly what this business requires. He doesn’t sell a scientific vision. He sells execution. And in a specialty with tight workflows and high-volume clinics, execution drives everything.

One pattern shows up across years of filings and earnings calls: Baum rarely frames decisions around short-term EPS or quarter-to-quarter optics. His focus is always on expanding the portfolio, strengthening the distribution base, and tightening the link between Harrow and the daily operations of cataract and retina practices. That long-term orientation explains why the company has been able to compound revenue through multiple transitions.

Evidence of Execution Discipline From Recent Commentary

Recent public remarks reinforce Baum’s pattern of candid assessment and corrective execution. At the Piper Sandler conference, he acknowledged that the first three quarters of 2025 for Triesence were a “disappointment,” citing launch missteps and strategic gaps inherited from prior owners. But he also highlighted leadership changes within commercial and strategic accounts that have already driven a visible turnaround. This willingness to confront issues directly, replace leadership, and correct course quickly aligns with the company’s decade-long operating rhythm.

Source: Piper Sandler Healthcare Conference (Triesence comments)

A Team Built for the Specialty

Harrow’s leadership team is unusually aligned around practical, clinic-level realities. Its commercial leaders come from ophthalmology or closely related specialties where volume, timing, and supply reliability determine success. The distribution, medical affairs, and practice-support teams are built to meet the needs of surgeons and ASC administrators who move hundreds of patients a week and cannot afford friction.

The team’s credibility with practices gives Harrow an advantage that portfolio size alone cannot buy: access. When Harrow introduces a new product, it doesn’t need to knock on cold doors. It is stepping into clinics that already trust the company.

Capital Allocation Discipline

Over the last decade, the company has shown a consistent willingness to acquire underappreciated branded assets that larger players no longer want to support. That discipline is grounded in three beliefs:

Harrow’s distribution footprint makes these assets more valuable internally than externally.

Reliable supply and predictable ordering can resurrect products that had been under-promoted or mishandled.

The company should prioritize products that strengthen its relationship footprint rather than chase unanchored scientific risk.

This capital allocation framework explains much of Harrow’s growth. Every acquisition has been small relative to traditional pharma deals, structurally de-risked, and immediately plug-and-play inside the existing commercial network.

Transparency and Communication

Harrow’s communications style is unusually direct for a company its size. Earnings calls do not read like marketing events; they read like operating updates. Management openly discusses supply dynamics, working-capital pressure, and the realities of portfolio integration. Even when results were messy — such as during heavy amortization periods — the company explained the underlying mechanics clearly.

This transparency is rare in small-cap healthcare, and it helps explain why the company has maintained investor support through capital-intensive phases.

The Real Test of a Management Team

Any leadership team can grow during the easy years. The real signal shows up when supply chains tighten, when working capital spikes, or when a company needs to integrate multiple branded products while scaling distribution. Harrow has already gone through those tests — and kept execution intact.

The next chapter will stretch the team again:

Melt-300 rollout, mix-shift expansion, debt service, working-capital normalization, and deeper integration across practices.

Nothing in the last decade suggests the team is unprepared for that challenge.

The Competitive Landscape Most Investors Misinterpret

The distinction matters. Companies like Alcon and Johnson and Johnson Vision build the highways of ophthalmology. Harrow operates on the side streets, intersections, and bridges where the day-to-day work actually happens. A surgeon may rely on Alcon’s phaco systems or Bausch and Lomb’s lenses, but Harrow supplies the products that surround every procedure. These include antibiotics, steroids, dilating agents, combination therapies, compounded formulations, perioperative workflow solutions, and soon a sedation platform through Melt-300.

A practice that adopts Harrow usually adopts more than one Harrow product, and the breadth of the branded suite reinforces this behavior.

The portfolio now spans inflammation, anesthesia, dry eye, anti-infectives, and legacy branded therapies acquired from multiple global manufacturers. This level of breadth is uncommon for a company of Harrow’s size and directly supports its ability to cross-sell across clinics and ASCs.

This positioning is a strength, not a weakness. Harrow operates in an area with very little competitive pressure because larger companies rarely allocate resources to support smaller SKUs across a fragmented specialty. Harrow’s advantage comes from its focus, operational discipline, and the distribution infrastructure that allows it to reliably serve thousands of practices that value consistency above all else.

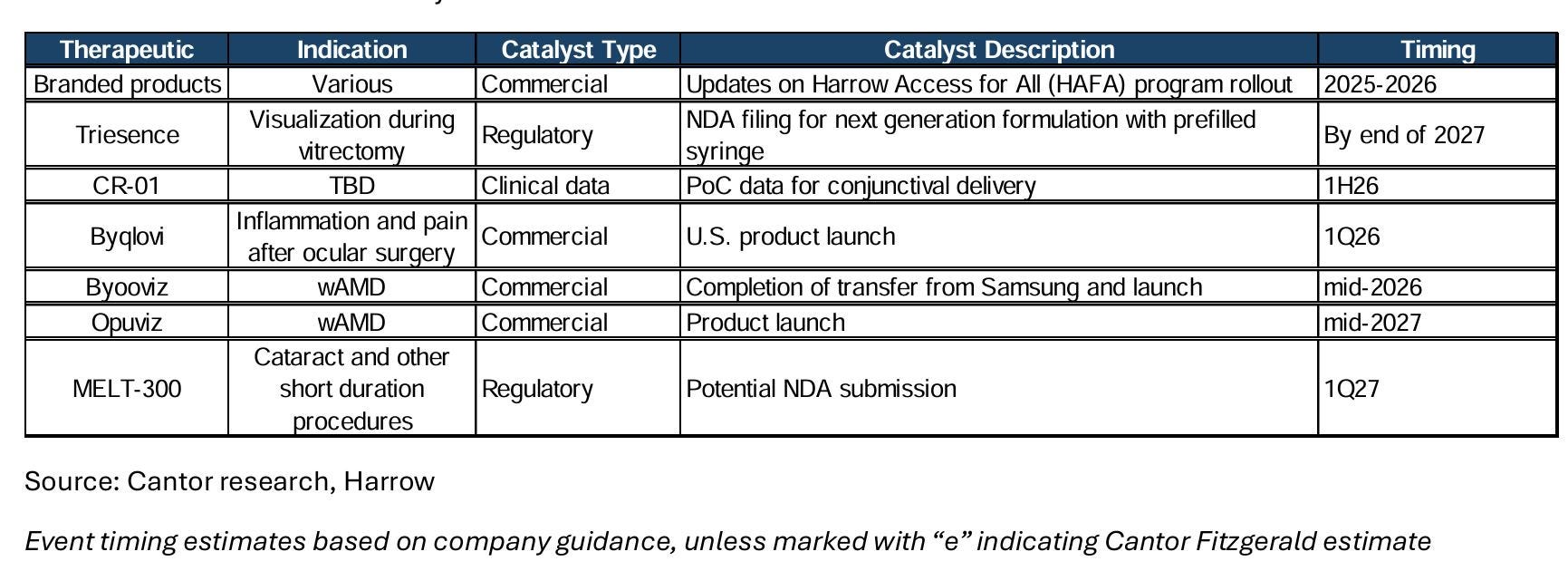

Harrow’s Upcoming Catalysts (Commercial + Regulatory)

Harrow’s strength is the breadth of its portfolio and the consistency of its product execution. The table below summarizes the most relevant commercial and regulatory catalysts across branded, compounding, and emerging pipeline assets.

These estimates come from a blend of company disclosures and third-party analyst research.

A few points stand out immediately.

The HAFA rollout expands Harrow’s logistical footprint.

Byqovi, Byooviz, and Opuviz provide incremental commercial leverage inside retina and cataract workflows. Most importantly, Melt-300’s potential NDA submission in 1Q27 marks the point where Harrow’s distribution engine and optionality layer intersect, which is the core of the long-term thesis.

A Practical Example of How Harrow Wins Inside a Practice

Consider a five-surgeon ophthalmology group performing roughly 250 cataract procedures each month, several hundred retina injections each week, and a steady daily flow of glaucoma visits. This profile is common across the United States, and practices of this size often operate at the edge of their scheduling capacity.

The pressure usually shows up in three places: inventory management, workflow coordination, and the unpredictability that comes from supply chain gaps. Any disruption in these areas can slow procedures, increase staff workload, and reduce the number of patients a practice can comfortably treat.

Harrow’s value becomes clearer when viewed through this lens.

1. Predictable delivery of compounded surgical formulations

Cataract surgeons depend on intracameral injections and specialized perioperative formulations. When these products arrive on time and with consistent quality, the surgical center stays efficient. When they do not, the entire operating day feels it. Harrow built its reputation by eliminating this source of friction.

2. Branded post-operative therapeutics that maintain reliable supply

Post-operative care flows more smoothly when products are consistently available. Staff spend less time explaining substitutions, patients experience fewer delays, and surgeons avoid callbacks triggered by pharmacy shortages. Reliable branded therapeutics reduce administrative noise for the practice.

3. Melt-300 as a solution to a core bottleneck

IV sedation remains one of the most common sources of slowdown in cataract surgery. It requires additional staff, more preparation time, and frequent adjustments. A practice that transitions to Melt-300 removes a significant operational constraint. Throughput improves, staffing flexibility increases, and cases move more predictably.

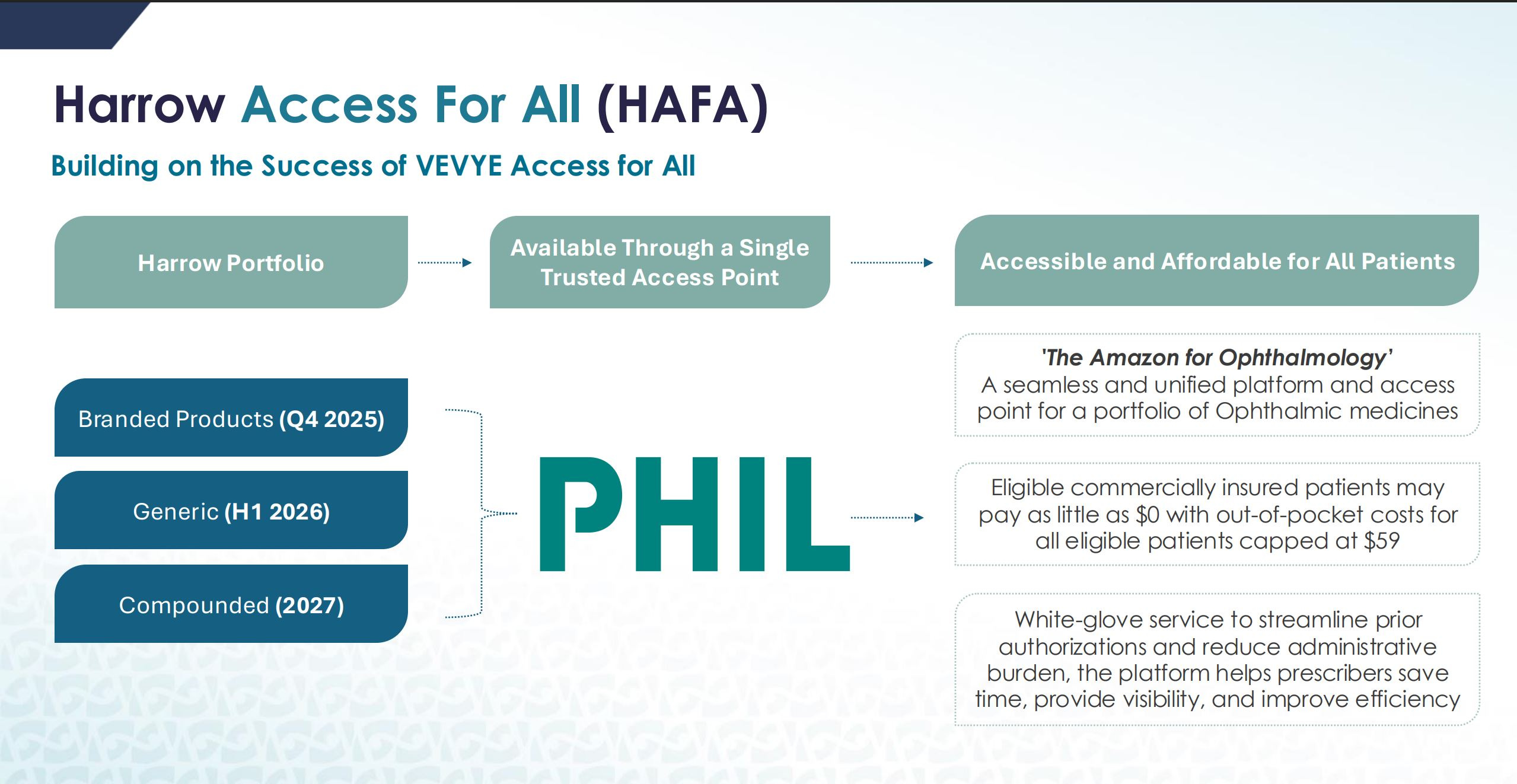

When a company addresses several points of friction within the same practice, it becomes difficult to replace. Ophthalmology groups rarely purchase isolated products. Once Harrow becomes integrated into the workflow, its access platform, HAFA, streamlines ordering, reimbursement, and inventory across branded, generic, and compounded items.

This is the underlying reason cross-selling works, and why Harrow tends to remain in place once established.

How Harrow Uses Portfolio Strategy To Deepen Its Competitive Position

At the conference, Baum described Harrow’s strategic posture not as a “single-product seller,” but as a provider of integrated perioperative and in-office solutions. In retina care, for example, Harrow now offers the anesthetic (IHEEZO), the anti-inflammatory (Triesence), and soon, biosimilars for Lucentis and Eylea. Each product reinforces the others in buy-and-bill settings, and the company’s commercial team — notably made up of former Regeneron veterans — is structured around these multi-touchpoint workflows rather than stand-alone brand teams. This approach fits the economic reality of retina and cataract practices, strengthening Harrow’s position where operational integration matters more than brand prestige.

Source: Piper Sandler Healthcare Conference (retina portfolio + biosimilar positioning)

Understanding Harrow’s Economic Model Through the Eyes of a Practice Manager

At the center of every ophthalmology practice is a practice manager or ASC administrator who functions as the operational leader of the business. This role carries responsibility for reducing friction, minimizing delays, coordinating inventory, protecting reimbursement, supporting surgeon productivity, and maintaining patient flow. Practice managers see the full machine and feel the impact of every vendor decision.

Harrow’s advantages become clear from that vantage point.

1. Product breadth simplifies vendor management

A practice manager would rather work closely with a few reliable partners than juggle a long list of vendors. Harrow’s expanding portfolio reduces the administrative load, creates fewer invoices, and consolidates communication into a smaller set of trusted relationships.

2. Compounding roots create deeper operational understanding

Compounding demands precision, reliability, and a high tolerance for complexity. Harrow earned loyalty during supply disruptions when many others struggled. Practices remember who kept them operating, and that memory translates into long-term trust.

3. Responsiveness is built into the company’s culture

Practice managers often describe Harrow as the partner that answers the phone and resolves problems quickly. In a specialty defined by high volume and tight schedules, responsiveness carries significant weight. It lowers the emotional and administrative cost of doing business.

4. Harrow reduces total operational cost

The true cost of a drug in ophthalmology extends beyond its price. Delays, rescheduling, patient dissatisfaction, and ASC bottlenecks all create hidden expenses. Harrow reduces these burdens. Investors often overlook this dynamic, but practice managers feel it immediately.

Why Growth Has Been Relentless and Why It Still Has Room

Many small-cap healthcare companies show a few years of momentum and then flatten. Harrow has not followed that pattern. The revenue path illustrates the consistency: roughly twenty million dollars in 2015, forty-one million by 2018, seventy-three million by 2020, one hundred thirty million by 2022, and two hundred fifty million today. Nearly thirteen-fold growth in less than a decade.

That trajectory is supported by three structural drivers that remain intact.

Driver 1: A broadening mix of branded products

The branded portfolio carries higher margins and greater operating leverage. This shift is possible because compounding creates the footprint, branded drugs scale inside that footprint, and each new product becomes cheaper to commercialize.

Driver 2: More portfolio depth means more touchpoints

Harrow is not positioned as a single-product company. It is a multi-touchpoint partner in a workflow-intensive specialty. Each new product strengthens practice reliance, raises switching costs, and expands economies of scale.

Driver 3: Melt-300 expands Harrow’s presence inside the operating room

Most ophthalmic drugs live in the clinic. Melt-300 lives in the surgical suite, which is the most influential part of the ophthalmic workflow. It offers higher visibility, higher operational impact, and a deeper form of trust. Even moderate adoption can reshape Harrow’s growth slope because it increases the company’s presence in the ASC, the economic engine of cataract surgery.

Why Investors Underestimate the Melt-300 Angle

The most common mistake in evaluating Melt-300 is treating it like a classic biotech event. Many frame it as a binary question about adoption, IV sedation replacement, or blockbuster potential. That framework misses the point entirely.

The better questions are operational. How much friction does the product remove from a cataract surgery day. How much throughput it opens up inside high-volume ASCs. How much staffing complexity it takes off the table. How many practices will try it simply because they already rely on Harrow for a significant portion of their workflow. How much additional pull-through it can generate for the broader portfolio. How effectively it deepens Harrow’s position inside the surgical suite.

Melt-300 is a workflow product. Its primary value is not in the revenue it generates on its own. Its impact comes from anchoring Harrow more deeply inside the ASC, strengthening practice-level loyalty, expanding cross-sell opportunities, and turning the portfolio from helpful to essential. That is why the product matters. The upside is not tied to blockbuster expectations, but to how it reinforces the flywheel already in motion.

What Most Analysts Miss About Harrow’s Financials

Harrow’s GAAP earnings naturally look messy because the company reports amortization from acquisitions, non-cash accounting adjustments, elevated commercial investment, and significant working capital movements. Traditional EPS screens struggle with this profile and often produce misleading conclusions.

Several financial realities tend to be overlooked.

1. GAAP net income is not the right lens today.

Amortization from acquired assets depresses earnings, which limits the usefulness of short-term EPS.

2. Working capital swings distort cash flow.

Rapid scaling increases receivables and inventory, which temporarily suppresses reported cash conversion.

3. Owner’s earnings provide a cleaner signal.

OE removes non-cash distortion, adjusts for temporary swings, and better reflects the underlying economic engine.

4. Branded mix expansion simplifies the financial profile.

As branded revenue becomes a larger share of the business, amortization becomes less impactful and cash flow improves.

5. Harrow is moving into a more profitable phase.

The company is shifting from a period of aggressive investment into a phase where operating leverage and cash conversion begin to show through.

Viewed through the wrong financial filters, the business can appear expensive. However, viewed through the correct ones, it often looks fairly valued or undervalued relative to its trajectory.

Why the Next Five Years Will Look Different From the Last Five

The last decade was about discovering and building the model. Harrow used that period to expand distribution, establish reliability, assemble a portfolio, and create a structure that could support multiple products at scale. That foundation is now in place.

The next five years will look different. This period is defined by stabilizing working capital, improving cash conversion, benefiting from operating leverage, rolling out Melt-300, adding assets selectively, increasing practice-level penetration, and shifting the revenue mix toward higher-margin branded products. The financial profile matures as these pieces come together.

This is the next phase of compounding, where the focus moves from building the model to harvesting the benefits of the groundwork already completed.

The Three Things Investors Should Watch Closely

Traditional earnings headlines will not tell the real story. The long-term signals are found elsewhere.

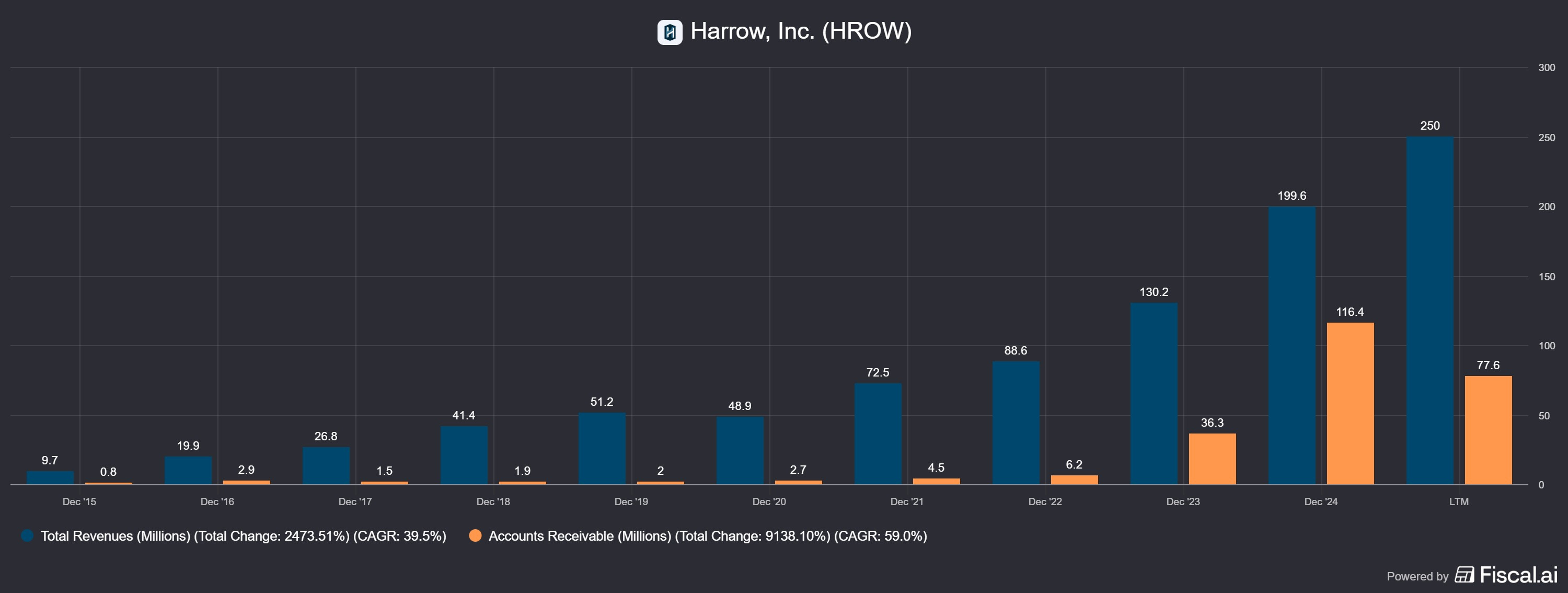

1. Working capital normalization.

Accounts receivable expanded rapidly during the scale-up period. Normalization over the next one to two years is both likely and necessary. It represents a key unlock for cash flow and is the most important near-term financial tension to track.

Chart: Harrow revenue (blue) vs. accounts receivable (orange). Rapid AR expansion during scale-up is visible, with early signs of normalization in LTM figures.

2. Branded mix growth.

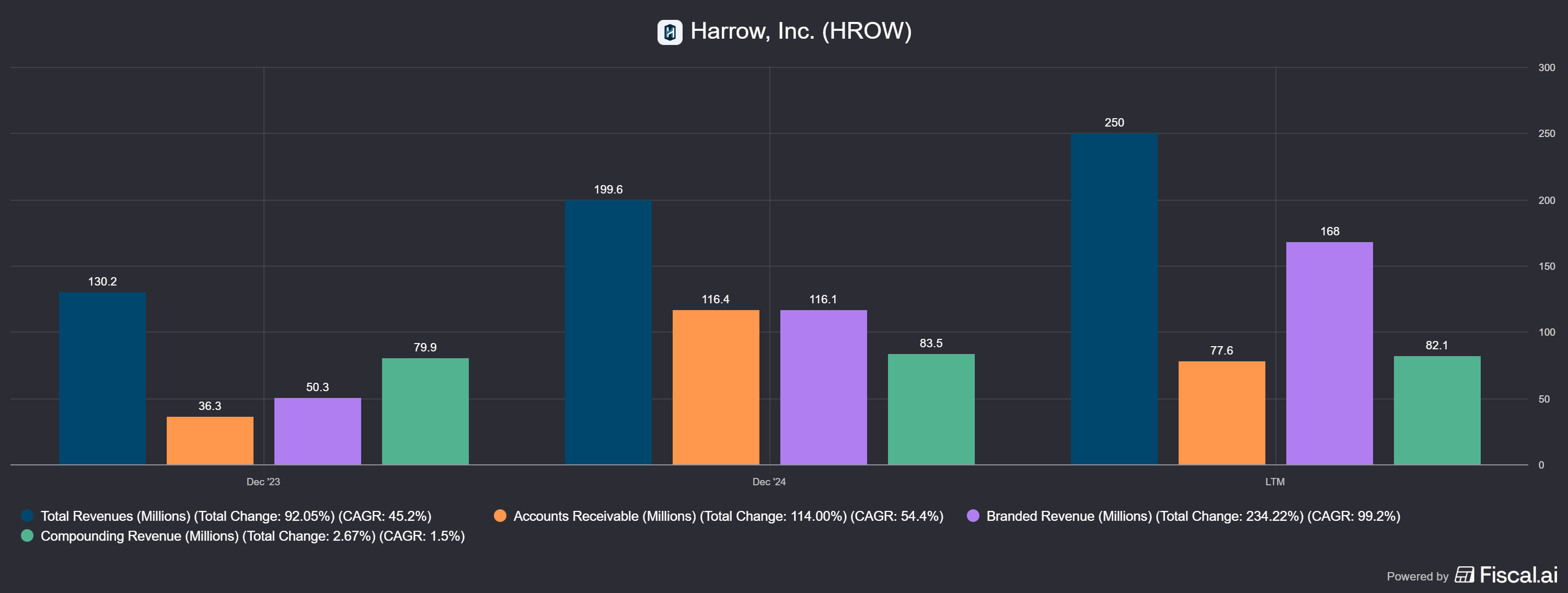

As branded revenue becomes a larger portion of the business, margins strengthen, cash flow stabilizes, and the company gains more flexibility to reinvest. A smooth progression here reduces many of the long-term concerns that appear in GAAP results.

Chart: Branded revenue now drives the bulk of Harrow’s growth, expanding from $50M to $168M in just two years. As branded mix rises, margins strengthen and the business becomes more predictable. The compounding base remains steady, but it is no longer the growth engine.

This is the first time branded revenue meaningfully exceeds compounding revenue, marking a decisive shift in the company’s economic model.

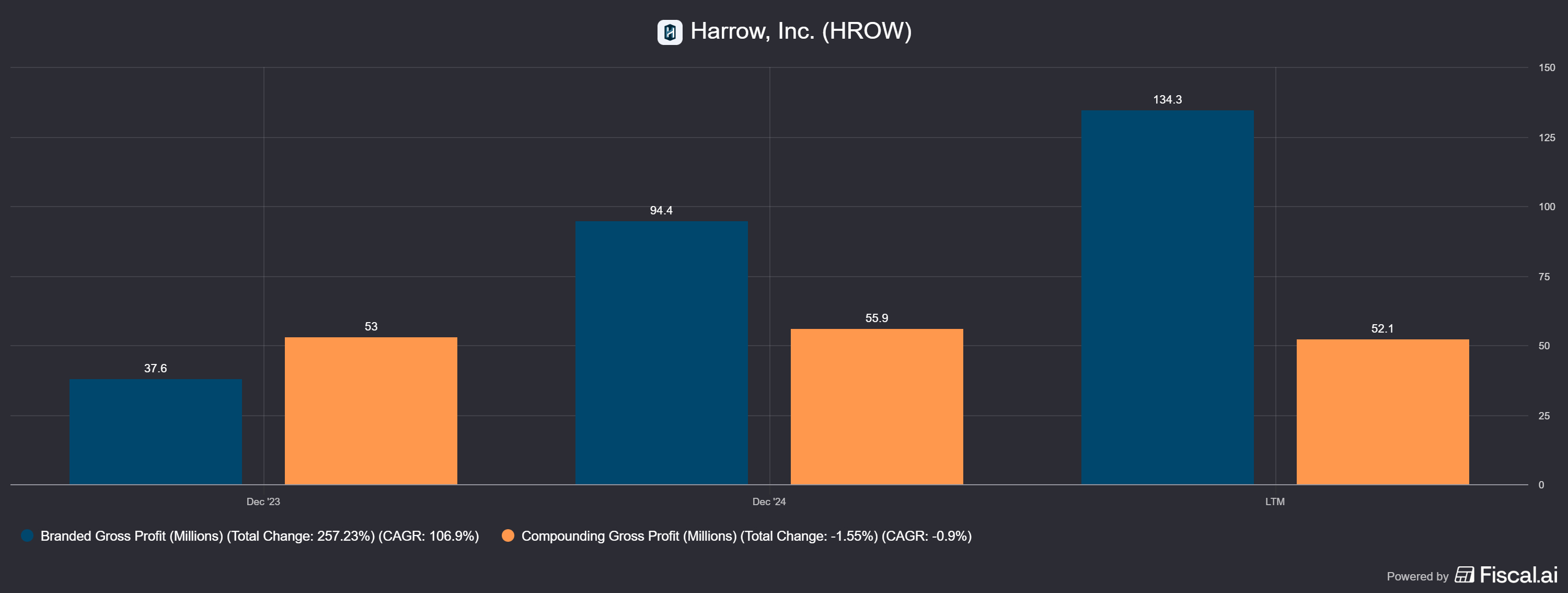

Chart: Branded vs. Compounding Gross Profit: Harrow’s Margin Mix Shift in Motion

Branded products are now the primary driver of gross profit, and the widening gap between branded and compounding margins shows exactly why the business becomes more predictable as the portfolio scales.

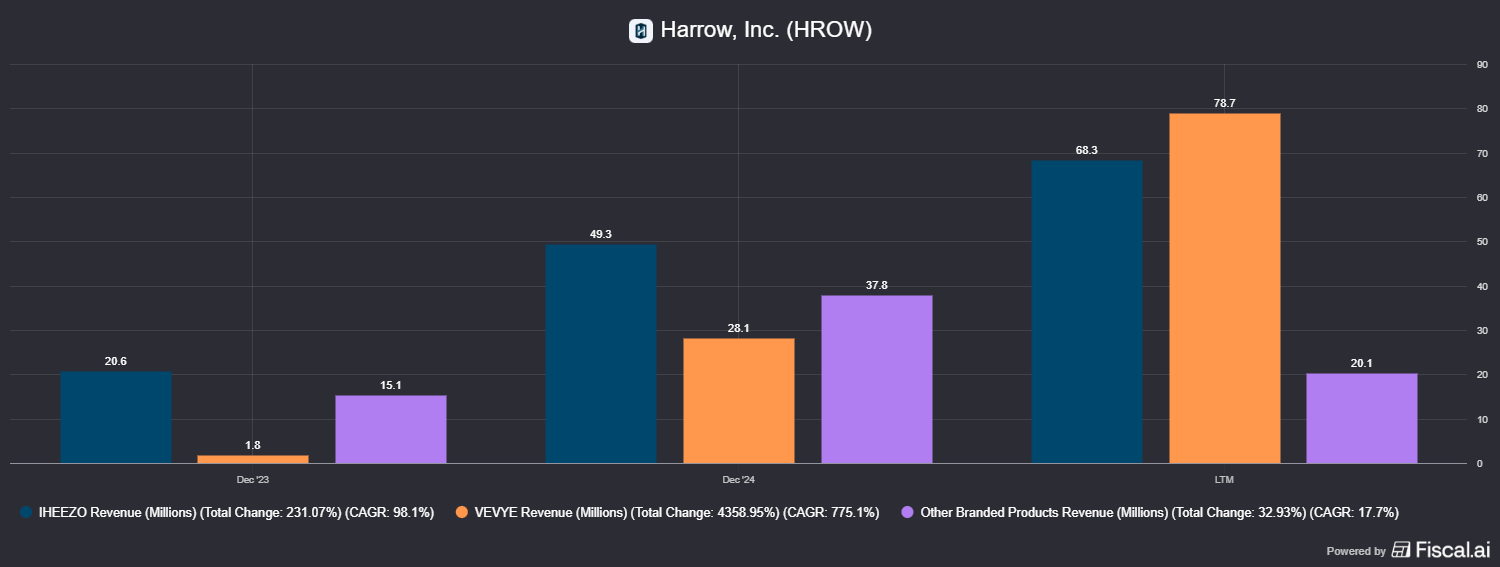

Chart: IHEEZO, VEVYE, and Other Branded Revenue Components

Growth in IHEEZO and VEVYE illustrates how Harrow turns under-supported ophthalmic brands into meaningful contributors once they are plugged into the company’s commercial footprint. The steep trajectory shows the effect of access, trust, and practice-level integration, and it demonstrates why additional branded assets often scale faster inside Harrow than they did under prior ownership.

3. Adoption and integration of Melt-300.

The product will not determine the entire investment thesis, but it can change the slope of long-term growth. Its impact on workflow, cross-sell leverage, and ASC integration is the variable worth watching.

3. Melt-300 Adoption Curve

IHEEZO is the closest analog for how Melt-300 could scale. Workflow products in ophthalmology tend to follow the same pattern: adoption starts slowly while clinics test and standardize, then accelerates quickly once friction disappears.

Not because Melt-300 must succeed, it doesn’t, but because the speed of adoption shapes the entire model. Too-slow adoption delays cross-sell benefits, moderate adoption strengthens the flywheel, and strong adoption changes the slope of long-term value creation.

The curve matters more than the total addressable market.

What Could Break the Thesis and How to Recognize It Early

Every investment has real risks, and Harrow is no exception. The good news is that the risks here are measurable, visible, and can be monitored long before they become structural.

The most important tension is simple: Harrow must execute while carrying meaningful leverage. If execution falters, the balance sheet becomes less forgiving. That is the core risk.

Early signs of trouble would include:

• Interest coverage slipping - Rising borrowing costs or slower operating growth would show up quickly in this ratio.

• Owner’s earnings flattening -If OE stops expanding while revenue keeps rising, it signals stress in the underlying model.

• Branded mix growth stalling -A stalled mix shift would weaken margin progression and slow the compounding engine.

• Receivables growing faster than revenue -A structural divergence here would indicate deeper working capital problems rather than temporary scaling effects.

• Practice-level adoption cooling - If surgeons and ASCs stop expanding their basket of Harrow products, the flywheel loses momentum.

• Reliability issues in distribution -Any sign of rising stockouts or inconsistent delivery would directly erode the trust that makes the business work.

• A materially slower Melt-300 rollout -Not thesis-breaking on its own, but a clear signal that the workflow impact is not landing as expected.

None of these red flags are visible today. Harrow’s momentum remains intact and the flywheel continues to build force. But these are the exact areas worth watching over the next several years because they tell the truth long before the headlines do.

The Real Harrow Story: A Final Synthesis

Stepping back from the details, the broader picture comes into focus. Harrow’s momentum has little to do with biotech excitement or hopes of a future blockbuster. The company is winning because it understands the daily reality of ophthalmology better than almost any peer in its weight class. Its strategy is built on the one thing that matters most inside a surgical specialty: the ability to make clinicians’ lives easier.

Harrow doesn’t position itself as a source of scientific miracles. It positions itself as the most reliable partner in a specialty where reliability is everything. Instead of chasing headline-grabbing drug innovations, it focuses on solving the operational friction that surgeons, ASC managers, and retina clinics deal with every day. Instead of talking about EPS first, it focuses on building trust at the practice level — and that trust turns into durable revenue.

This is how Harrow grew from roughly $20M in revenue to more than $250M in under a decade. It did it by expanding into multiple points of the ophthalmic workflow, one product and one relationship at a time. Melt-300 has the potential to strengthen that position, but it is not the foundation of the story. The real driver is Harrow’s ability to earn, keep, and deepen its role inside busy practices that cannot afford disruption.

The company isn’t behaving like a hype-driven biotech swinging for a moonshot. It isn’t a fragile one-product business hoping that one launch carries the entire valuation. And it isn’t a roll-up collecting assets for the sake of appearances. Harrow is building a position inside one of medicine’s most procedural, time-sensitive, and operationally demanding specialties. The strategy is simple: expand access, widen the portfolio, reduce friction, and become indispensable.

That’s the part of the story most investors overlook. Once Harrow is integrated into a practice, it tends to stay. That dynamic, not Melt-300 alone, not any single acquisition, not any one quarter, is what makes the next decade so compelling.

Part 1 lays out how the business actually works, the flywheel, the workflow positioning, the risks, and the structural drivers that shaped Harrow’s first decade. Part 2 shifts from narrative to numbers: owner’s earnings, reverse DCFs, valuation scenarios, and a grounded view of long-term return potential. It’s where all the threads come together.

Part 1 lays out how the business actually works, the flywheel, the workflow positioning, the risks, and the structural drivers that shaped Harrow’s first decade.

Part 2 shifts from narrative to numbers, focusing on owner’s earnings, valuation scenarios, and what the current stock price already assumes.

Disclaimer

The information in this article is provided for informational and educational purposes only.

The information is not intended to be and does not constitute financial advice or any other advice, is general in nature, and is not specific to you. Before using this article’s information to make an investment decision, you should seek the advice of a qualified and registered securities professional and undertake your own due diligence.

None of the information in this article is intended as investment advice, as an offer or solicitation of an offer to buy or sell, or as a recommendation, endorsement, or sponsorship of any security, company, or fund. The author is not responsible for any investment decision made by you. You are responsible for your own investment research and investment decisions.

Thank you all for requesting Part 2. For those who subscribed as well, Part 2 is in your inbox. For those who have only commented, feel free to DM me with your email so I may send it along. I may have messaged you already requesting.

Keep Moving, TuDi

Interested, thanks. Interested in part 2 as well.